Blur, the current market-leading NFT marketplace, recently announced a new peer-to-peer NFT lending platform: Blend.

What is Blend?

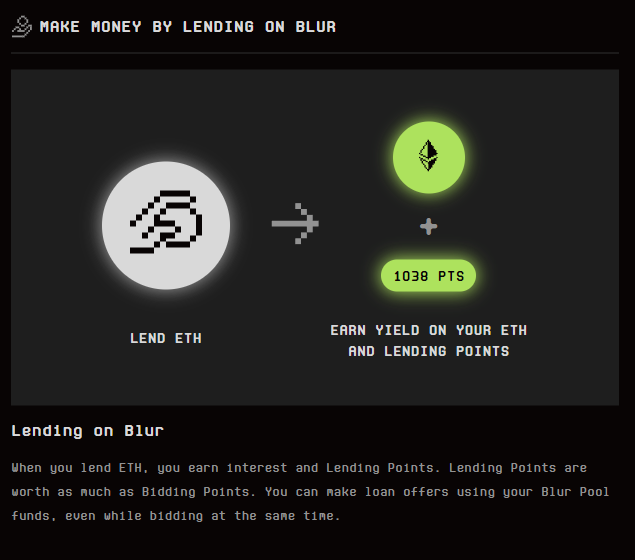

Blend allows users to borrow and lend using non-fungible tokens (NFTs) as collateral.

Lenders can offer loans with their chosen interest rates and terms, while borrowers can repay the loans or face the liquidation of their NFTs if the lender decides to exit the loan.

The key features of the Blend platform are:

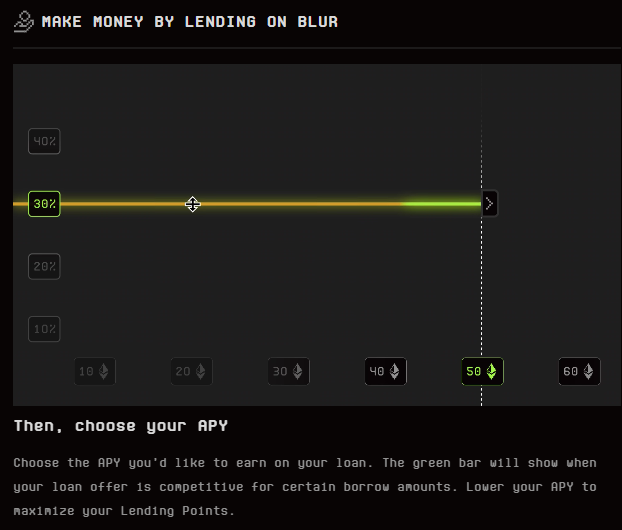

No oracles: Blend does not rely on oracles, which are external data sources (an example would be a property surveyor in the housing market), to determine the value of NFTs or to set interest rates. Instead, the market participants decide on these factors.

No expiries: Loans on Blend do not have a fixed end date. They can continue indefinitely until the borrower repays the loan or the lender decides to exit the position.

Liquidatable: If a lender wants to exit a loan, they can trigger an auction to find a new lender. If no new lender is found, the borrower's NFT is liquidated, and the lender takes possession of it.

Peer-to-peer: Blend operates as a platform where individual loans are matched between users, rather than pooling funds like other platforms.

Examples of such arrangements are the ability to borrow up to 42 ETH against your Crypto Punk or buy that typically out-of-reach 15 ETH Azuki for only 2 ETH (with a 13 ETH loan).

Credit: @blur_io

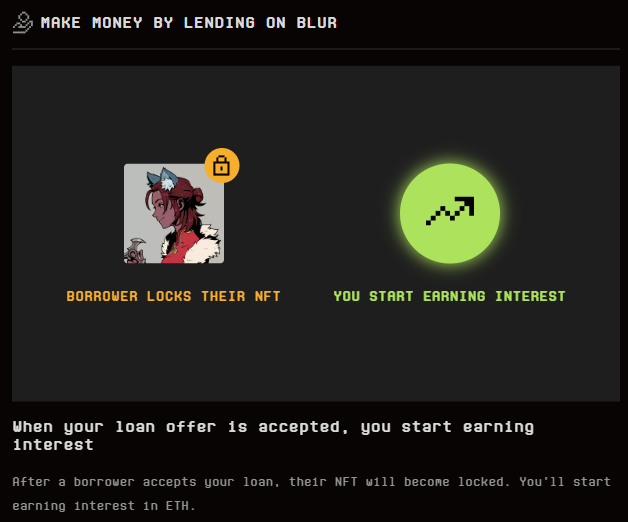

Lenders simply select their Max Borrow, their APR and start earning when the loan is accepted by a user, locking the NFT until the loan is repaid.

Credit: blur.io

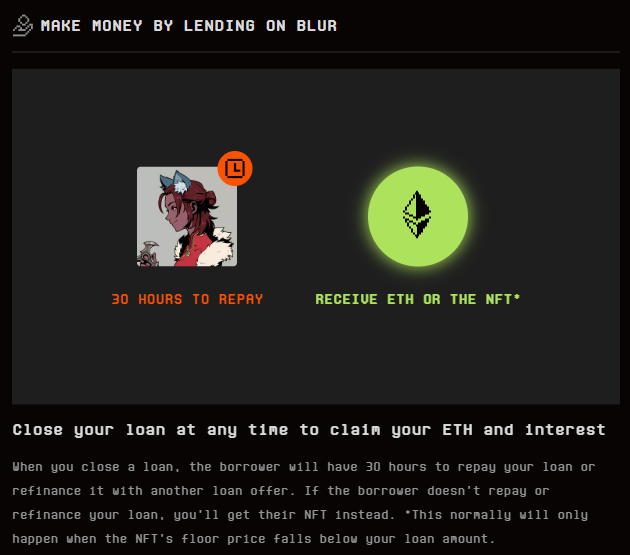

When a lender wants to close the loan, they can do so at any time to claim the ETH loan back and interest. The borrower has short 30 hours to repay, either through self-funding or refinancing.

If they don't repay within 30 hours, the lender takes possession of the NFT.

Credit: blur.io

Blur compares Blend to mortgages

Blur bizarrely compared their new Blend platform to mortgages, stating that "every trillion dollar market relies on financialization to scale. NFTs are no different".

4/ Every trillion dollar market relies on financialization to scale. NFTs are no different.

Instead of paying $1m for a house, buyers put $100k down and pay the rest through their mortgage. Without this mechanism, almost no one would be able to afford homes. pic.twitter.com/4J96G3pGnJ

Kudos to the brilliant @HashBastardsNFT for first bringing this to light through his tweet. Be sure to follow him for a delightful blend of insightful and humorous takes on the NFT world.

Comparing Blend to mortgages presents an intriguing analogy; however, upon closer examination, this comparison falls short of capturing the true nature of the platform.

The attempt to instil confidence in potential users by drawing parallels to a familiar financial instrument, such as mortgages, may even be considered reckless.

The risks associated with NFT investing differ significantly from those of traditional mortgage lending, and it is essential to acknowledge and understand these distinctions rather than relying on superficial similarities.

Aside from collateral-backed loans, liquidation of the collateral and interest rates, there are very few similarities.

Key Differences

Nature of collateral: Mortgage lending uses real estate properties, which have a more established and widely accepted valuation process, whereas NFTs are highly volatile, speculative assets.

Oracle dependency: Mortgage lending relies on appraisals, credit scores, and other external data sources to determine the value of the collateral and the borrower's creditworthiness. As explained above, Blend has no oracles, placing this responsibility on market participants (i.e. the lenders/borrowers).

Loan duration: Blend's perpetual loans have no expiry, and borrowing positions can remain open indefinitely. Mortgage lending, on the other hand, usually has fixed loan terms, such as 15, 20, or 30 years. A mortgage lender can also not close a loan with 30 hours' notice.

Loan model: Blend operates on a peer-to-peer model, matching individual loans between borrowers and lenders. Mortgage lending typically involves financial institutions or mortgage brokers that pool funds and manage risks on behalf of multiple investors.

Regulatory environment: Mortgage lending is heavily regulated in most jurisdictions to protect both borrowers and lenders. Blend's NFT-backed lending operates in a nascent and unregulated space, which could pose additional risks and uncertainties for both parties.

It could be argued that Blur's comparison of Blend to mortgages was simply an attempt to convey the idea that financial instruments are necessary for scaling. It certainly will provide liquidity and encourage transactions that otherwise wouldn't be possible.

However, using mortgages as an example is certainly at the least misguided, as it does not accurately reflect the risks and nuances involved in the Blend platform, and could potentially mislead market participants into a false sense of security.

Blend: mortgage a house of cards?

Blur's Blend platform certainly has the potential to create a speculative bubble, with the likely many ill-informed market participants on both the lending and borrowing sides, which could result in a panic-driven collapse when the bubble bursts.

Risks for Lenders:

Lack of reliable valuation: Unlike real estate, NFTs are highly volatile and lack standardized valuation methods, making it difficult for lenders to accurately assess the worth of the collateral. This could lead to lenders extending loans against overvalued assets, putting their capital at risk.

Insufficient collateral: If the NFT market experiences a sudden downturn or the value of the collateral drops significantly, lenders may find themselves unable to recoup their loan principal and interest, resulting in losses.

Illiquidity: In the event of a market collapse, lenders may struggle to sell the NFT collateral they have acquired through loan defaults, further exacerbating their losses.

Risks for Borrowers:

Over-leveraging: The speculative nature of the NFT market, coupled with the allure of easy borrowing, may encourage borrowers to over-leverage themselves, putting their NFT assets at risk of liquidation in the event of a market downturn or inability to refinance.

Interest rate fluctuations: Borrowers could be exposed to interest rate fluctuations without a fixed loan duration, making it difficult to manage their financial obligations.

The 30-hour window: The narrow 30-hour window for repaying or refinancing a loan when a lender decides to close puts tremendous pressure on borrowers, who may struggle to secure the necessary funds or find another lender within this short timeframe. This increases the risk of losing their NFT collateral.

Predatory behaviour: The short window could also incentivise predatory behaviour among lenders, who might strategically choose to close loans at opportune times, putting undue pressure on borrowers and increasing the likelihood of defaults and collateral acquisition (especially group-led coordinated closures).

In reality, the Blend platform presents a host of risks to both lenders and borrowers that are significantly different from those associated with traditional financial tools such as mortgages.

While the concept of Blend's peer-to-peer NFT lending platform may appear intriguing and even groundbreaking, one could argue that it is simply another form of gambling disguised as a financial tool, potentially encouraging reckless behaviour among untrained market participants.

As the NFT market continues to evolve and mature, it is crucial for all parties involved to tread carefully and consider the potential risks in this speculative space.

I love retro and being at the cutting edge, always willing to give time and thought to anything and everything. Arodie is an extension of me, exploring all corners of Pop Culture collectibles.

Join Funko on May 28, 2024, at 11 AM PT / 2 PM ET for the launch of the Scooby-Doo Funko NFTs Series 2. Discover all you need to know, including the new Ultra rarity!